“IEA: Coronavirus ‘accelerating closure’ of ageing fossil-fuelled power plants“

Josh Gabbatiss, Carbon Brief, 27 May 2020

***

This year will see the largest ever drop globally in both investment and consumer spending on energy as the coronavirus pandemic hits every major sector, according to the International Energy Agency (IEA).

The crisis is accelerating the shutdown of older fossil-fuelled power plants and refineries, with the agency saying it could provide an opportunity to push the global energy sector onto a “more resilient, secure and sustainable path”.

In the latest edition of the World Energy Investment report, which Carbon Brief has covered in previous years, the IEA has gone beyond its usual remit of reviewing annual trends.

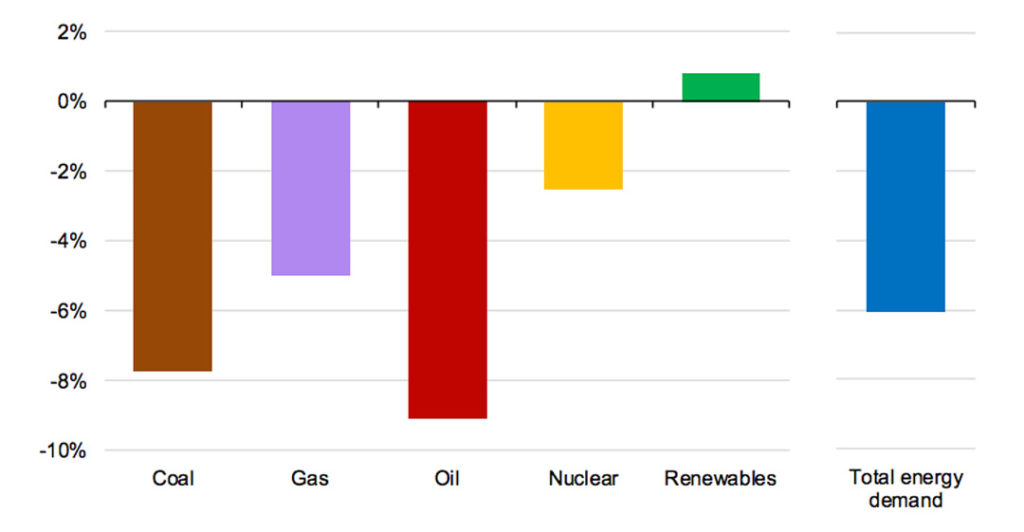

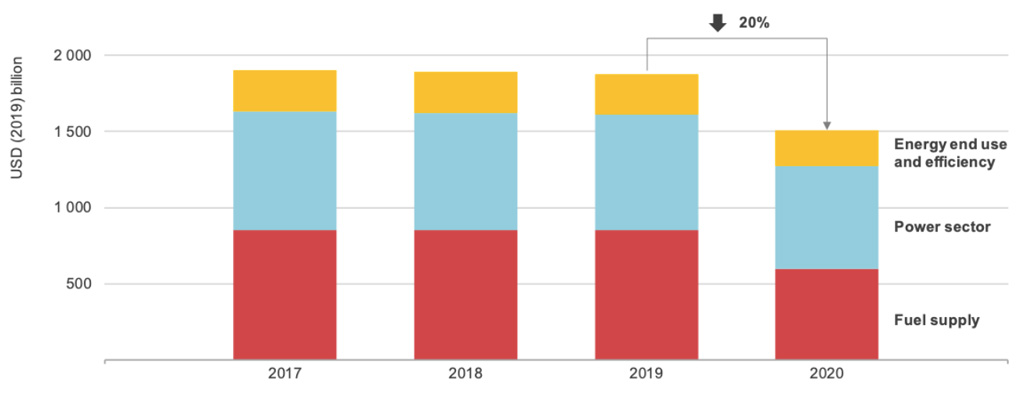

Its analysis looks ahead to the coming year and estimates the impact of this year’s economic turmoil on energy investment, which was expected to grow by around 2% prior to Covid-19. It is now expected to drop by 20%, or almost $400bn.

Meanwhile, as demand and prices collapse, consumer spending on oil is expected to drop by more than $1tn, prompting a “historic switch” as spending on electricity exceeds oil for the first time.

Here, Carbon Brief has picked out some key charts to illustrate the economic repercussions of the pandemic across the energy sector.

Energy investment will drop by a fifth

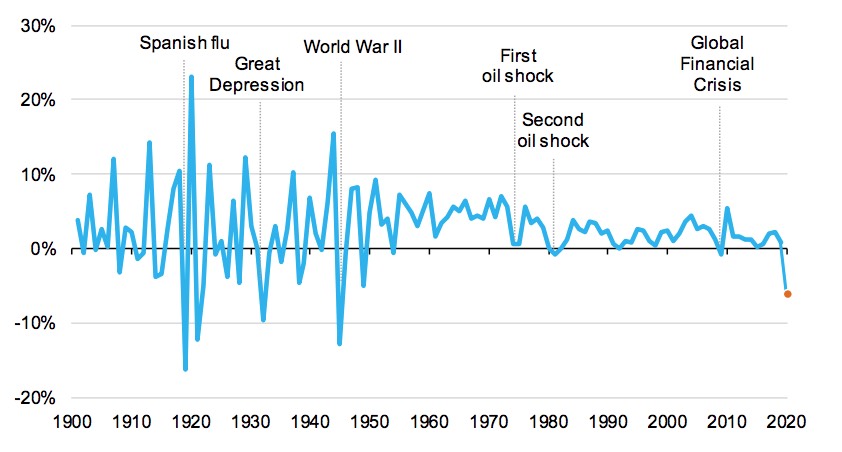

The “baseline expectation” for 2020 is a global recession resulting from widespread lockdowns, according to the IEA. Last month, the agency estimated this will also lead to CO2 emissions dropping by 8% this year in the largest decline ever recorded.

Based on the latest investment data and project information, announcements from companies and governments, interviews with industry figures and its own analysis, the IEA concludes such a recession will see energy investment drop by a fifth. This can be seen in the chart below.

These estimates are based on assumptions about the duration of lockdowns and coronavirus recovery trajectories.

The IEA notes that “almost all” investment activity has been disrupted by these measures, as a result of restrictions to the movement of people, goods and equipment.

However, the largest impacts are the result of declines in revenues due to falling demand and prices, with the clearest example coming from the oil sector. Analysis of daily data until mid-April suggests countries in full lockdown have seen energy demand drop by a quarter.

As a result, the agency also estimates that these factors, combined with a rise in cases of people not paying their energy bills, will see revenues going to both governments and industry fall by over $1tn this year.

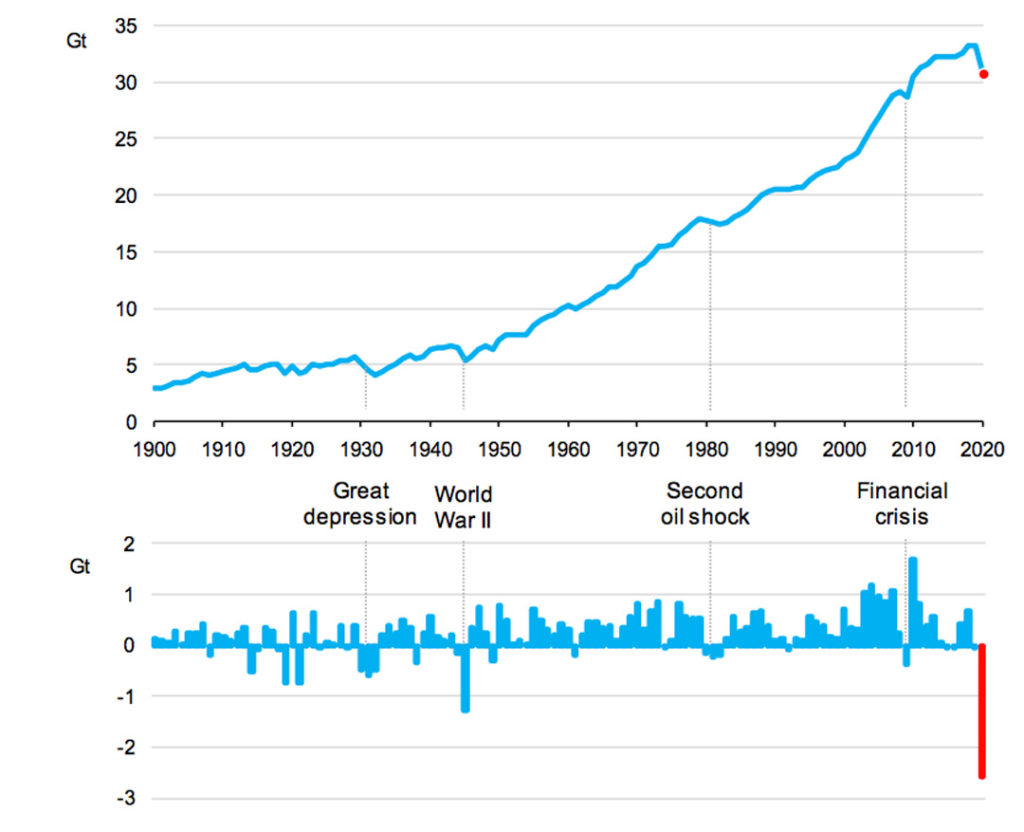

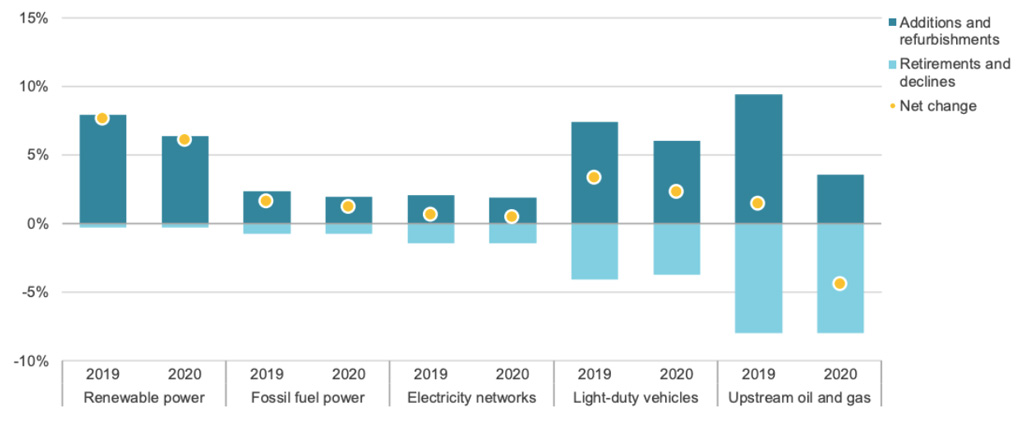

Crisis ‘accelerating’ shift from low-efficiency technologies

Every year energy infrastructure is retired and replaced with new equipment. Typically, the replacement technologies will be cleaner and more efficient, although this is not always the case.

The coronavirus crisis is expected to have an impact on this rate of turnover and, indeed, it is already contributing to the retirement of some older power plants and facilities, as the chart below illustrates.

The economic downturn and “surfeit of productive capacity in some areas” as overall demand plummets is already “accelerating” the closure and idling or inefficient technologies, including refineries and some coal-fired power plants.

However, the IEA warns that equally governments might respond to the pandemic by underinvesting in new technologies and remaining reliant on inefficient, older technology. The agency estimates efficiency investment could drop by 10-15% as spending is cut back.

The report warns that policymakers should keep these elements in mind and “combine economic recovery with energy and climate goals”. Dr Fatih Birol, executive director of the IEA, said in a statement that while the pandemic has brought lower emissions it has been “for all the wrong reasons”:

“The response of policymakers – and the extent to which energy and sustainability concerns are integrated into their recovery strategies – will be critical.”

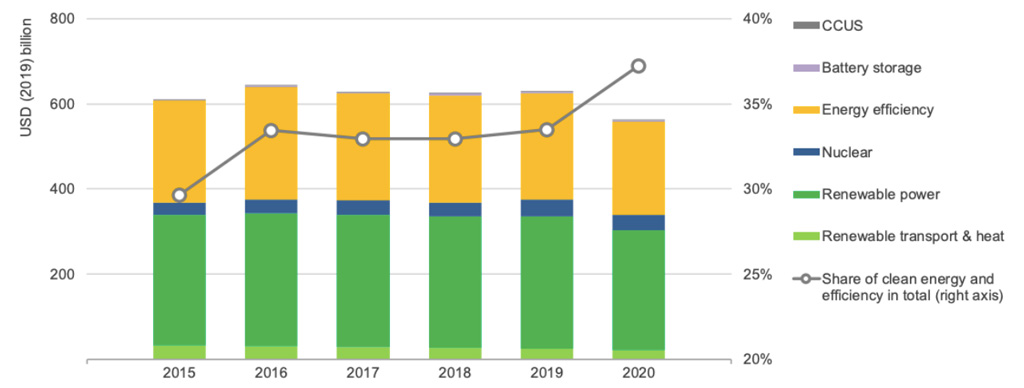

Clean energy spending ‘relatively resilient’

The share of global energy spending going towards clean energy, including renewables as well as nuclear and efficiency improvements, has been flat-lining at around one-third for the past few years.

As the chart below shows, this is likely to change this year as clean energy’s share edges closer to two-fifths of overall spending.

Clean energy investment is expected to remain “relatively resilient” this year, with spending on renewable projects falling by a comparatively small 10%.

However, according to the IEA, the main reason for clean energy increasing its share is that fossil fuels are set to take such a “heavy hit”. In absolute terms, spending on these technologies is “far below levels” required to accelerate energy transitions.

The agency notes that investment trends have long been “poorly aligned” with the world’s needs and are still set to fall short of the future it has outlined in its benchmark Sustainable Development Scenario (SDS).

Last year’s edition of the World Energy Investment report concluded that investment in low-carbon energy sources must more than double by 2030 if the world is to meet its Paris Agreement targets.

While the slowdown in clean energy spending is less significant, it still “risks undermining the much-needed transition to more resilient and sustainable energy systems,” according to Birol.

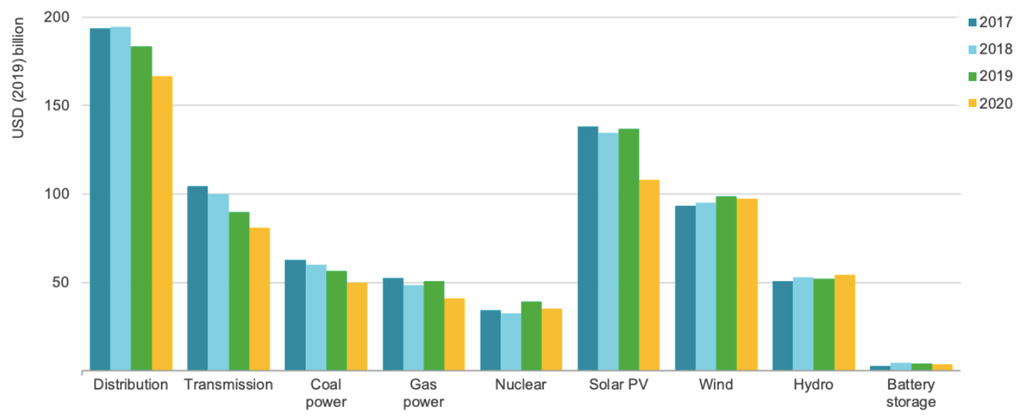

Power sector hit hard

International power investment is set to drop by 10% as a result of the Covid-19 pandemic, according to the agency.

Virtually every component of the sector is expected to see a decline in investment, with hydro the only exception, as the chart below demonstrates.

Increases in residential electricity demand around the world during lockdown are being “far outweighed” by reductions in commercial and industrial operations, the agency reports. A 9% decline in spending on electricity networks this year is also expected.

The IEA says some parts of power investment are more exposed, specifically fossil fuel-based generation.

Meanwhile, higher shares of renewables are being dispatched due to low operating costs and priority access to networks. Nevertheless, renewables are still taking a hit, particularly distributed solar photovoltaics (PV) as households and companies cut back on spending.

Technologies with a longer lead time, notably offshore wind and hydropower, are expected to do better despite some delays.

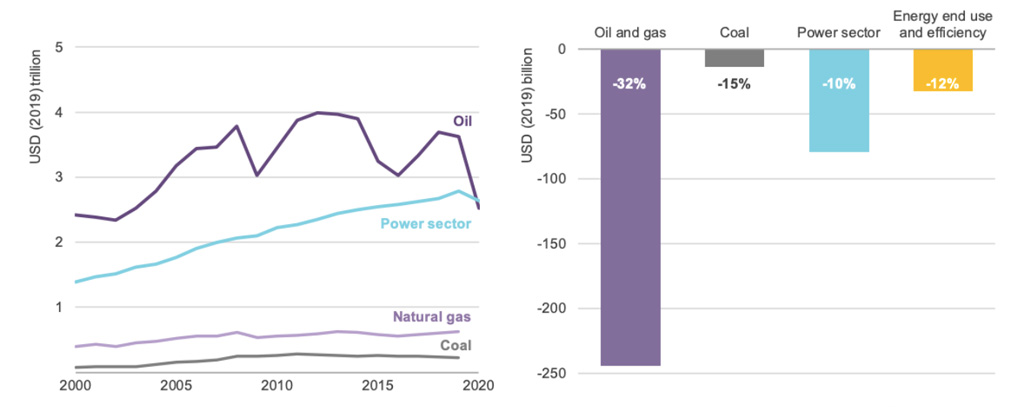

Electricity spending pulls ahead of oil

Oil accounts for most of the decline in revenues expected this year. Furthermore, in a “historic switch” consumer spending on electricity could exceed spending on oil for the first time ever.

While power-sector revenues are expected to fall by $180bn, oil spending will likely drop by at least $1tn. This can be seen in the chart on the left below. Taken together, investment in oil and gas is expected to fall by almost a third in 2020.

The decline in aviation and road transport, which represent nearly 60% of oil demand, are responsible for this disproportionate decline.

Meanwhile, the impact on gas has so far been more moderate, but could fall further due to reduced demand in power and industry settings.

The report also highlights the global shale sector, which was already under pressure, as being particularly vulnerable.

With investor confidence and access to capital in decline, the IEA predicts shale investment will halve in 2020 and notes the outlook for “highly leveraged shale players in the US” is now “bleak”.

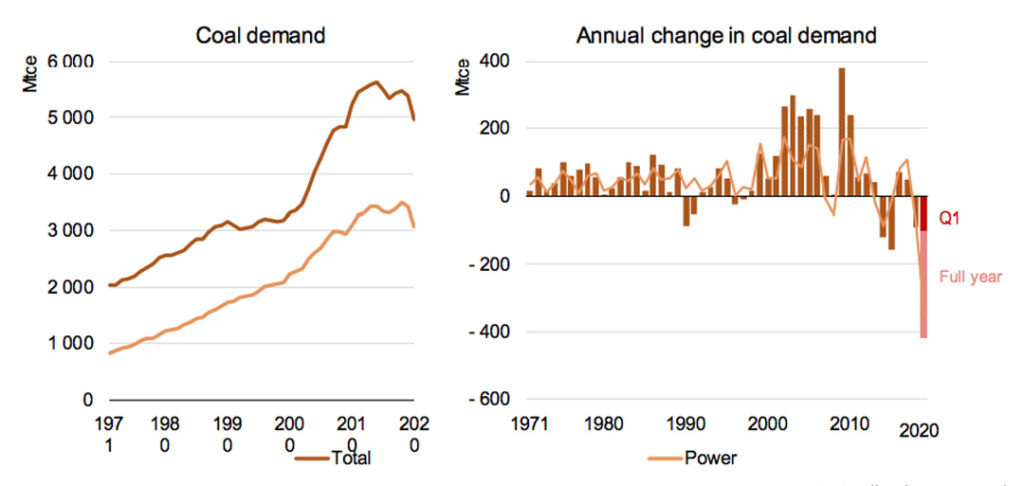

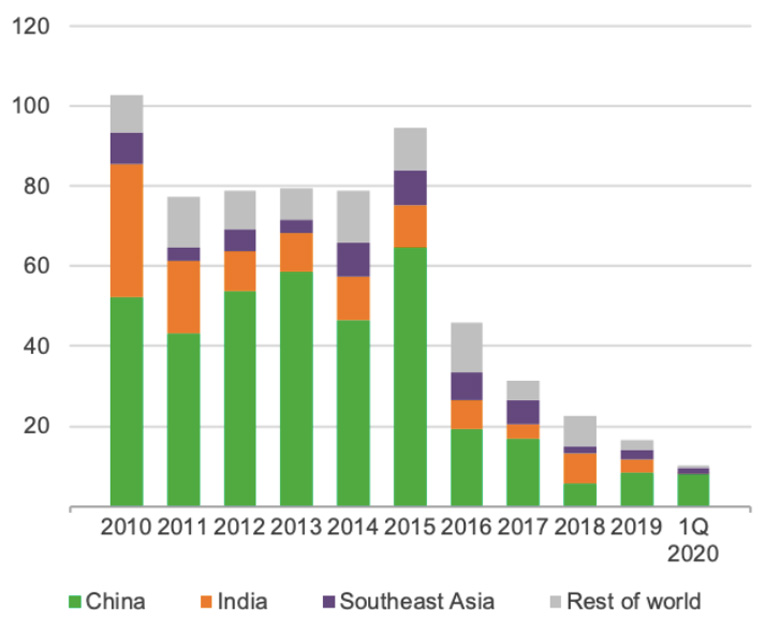

Coal decline given a ‘floor’ by China

Coal is estimated to be the fuel hardest hit by the crisis after oil. Coal demand could drop by 8% this year, investment in coal supply is set to fall by a quarter and spending on new coal-fired plants is set to fall by around 11%.

However, any decline in coal’s fortunes may be curtailed by the recovery of demand for the fossil fuel in China. According to the IEA, investment activity there “may put a floor” under further reductions in coal-power investment this year.

The nation’s focus on coal is illustrated in the chart below, which shows final investment decisions (FIDs) dropping to their lowest levels in a decade, but China providing virtually all of them in the year so far.

Using data available so far, the IEA notes that approvals for new coal plants in the first quarter of 2020, were “running at twice the rate observed over 2019 as a whole”, primarily in China.

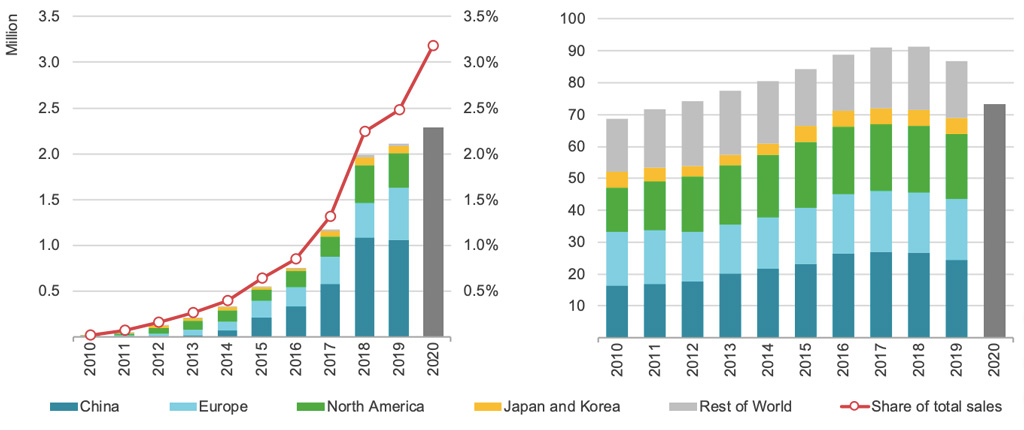

Electric vehicle sales rising as overall market contracts

Last year was a difficult time for the car industry, with total sales growth slowing in all major regions and turning negative in China and the US.

However, this “turbulent” period for the industry is “likely to appear mild” in comparison with 2020, according to the IEA.

Lockdowns have already severely impacted sales and, across the year, the agency estimates a drop of around 15% – dramatic even compared to the 10% drop that followed the 2008 financial crisis. Negative trends in overall car sales can be seen in the right-hand chart below.

However, even though electric vehicle sales followed wider patterns and stalled in 2019 largely due to declining Chinese purchases, their overall market share continued to climb.

This can be seen in the chart on the left, which shows that electric cars are expected to go against the broader trend in 2020. The IEA estimates that owing to policy support, particularly in Europe, electric vehicle sales will increase this year, as will their share of the market (indicated by the red line).

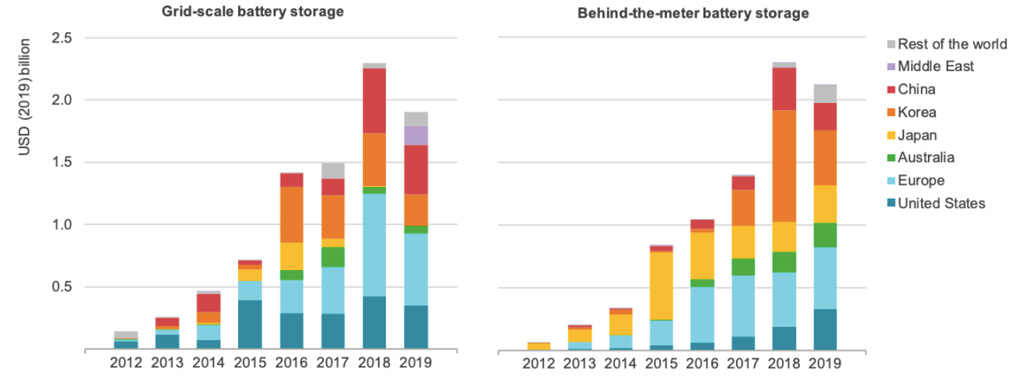

Battery storage spending fell as prices dropped

Investment in battery storage fell for the first time last year, as the chart below shows. Overall, spending on grid-scale and behind-the-meter batteries fell by 15%, with overall investment just above $4bn.

The IEA states this decline took place as costs for battery storage fell rapidly, a trend the agency attributes to maturing supply chains and markets, more efficient production and competition within the sector.

The report mentions fires at energy storage installations in South Korea and regulation uncertainty in China as some of the factors behind the decline in interest last year.

Declining behind-the-meter battery spending also reflects the distributed solar PV market, for which investment slowed last year in a trend expected to continue as consumer spending drops off due to coronavirus.

The agency notes that grid-scale battery investments are also expected to decline this year against the backdrop of a general decrease in power activity.

However, it says this setback “is likely to be shortlived” due to the technology’s growing importance for system security and flexibility.

***

“IEA: Coronavirus ‘accelerating closure’ of ageing fossil-fuelled power plants“

Josh Gabbatiss, Carbon Brief, 27 May 2020

Published under a CC license. Carbon Brief welcomes the reproduction of unadapted material in full for non-commercial use, credited ‘Carbon Brief’ with a link to the article.